Most Popular

-

1

Opposition-led Assembly unilaterally passes bill to probe Marine's death

-

2

Golden chance to liquidate babies’ gold rings?

-

3

Inflation eases in April, continues bumpy ride

-

4

Russia sent more than 165,000 barrels of refined petroleum to N. Korea in March: White House

-

5

Seoul to more than double military drones by 2026 to counter NK threats

-

6

Key suspects grilled over alleged abuse of power in Marine death inquiry

-

7

Seoul alerts overseas missions to NK terror threats

-

8

Over 60% of S. Koreans support W100m childbirth incentive: survey

-

9

‘Inside Out 2’ adds four new emotions, explores teenage life

-

10

Questions raised over fair promotion of RM, NewJeans

By Steve Brice

In financial markets, there is an inherent tug-of-war between themes/stories and valuations. We are seeing one play out in the equity markets right before our eyes, in the semiconductor industry. This reminds me of my formative investment years of the late 1990s. While we should not blindly follow historical examples, this comparison is something for investors to bear in mind when it comes to making financial decisions and sizing investment positions.

Let me start with a caveat. I am not a stock picker. It is incredibly difficult to consistently pick stocks that outperform. This is borne out by the difficulty fund managers have in outperforming their benchmarks over the long term, especially in the more developed, liquid and efficient markets. Therefore, this article is meant to be more thought-provoking rather than implying an outlook for the stocks mentioned.

In the late 1990s, the internet was the craze. Truly incredible things were happening. Adding ‘.com’ to the name of your company could lead to a significant revaluation of your stock prices, seemingly disregarding any changes to your business model. Indeed, a privately owned company I worked for at that time did exactly that, sparking speculation internally that the owners were looking to sell the company.

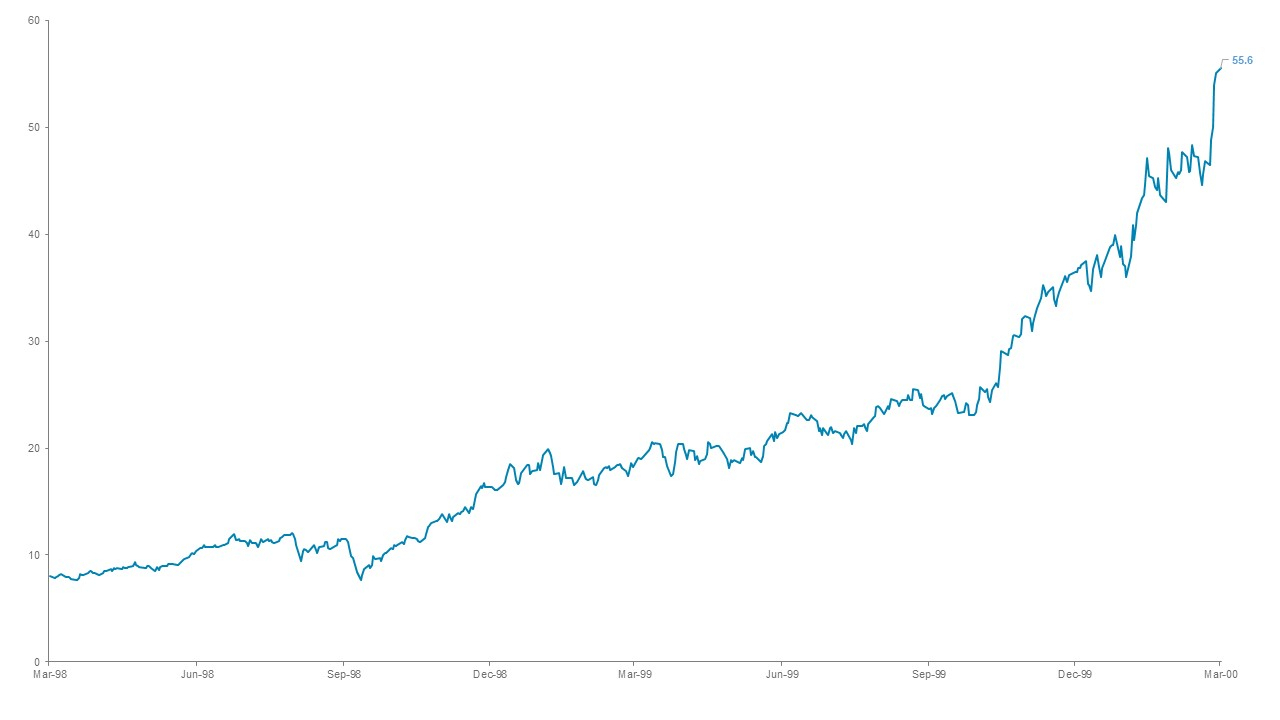

There were, of course, companies that actually did have strong internet-focused business models and a very strong competitive advantage. One such company was Cisco Systems, a company that built networks upon which the internet was based. Unsurprisingly, given the hype and its positioning, the stock performed extraordinarily well. At its peak in March 2000, Cisco traded almost seven times the price of just two years earlier.

Cisco System’s share price soared in the late 1990s during the internet bubble

Thereafter, the stock price took a significant downturn, falling 83 percent in the next three years. The impact was not just short-term. From its peak on the 27 March 2000, it took until September 2021 for the stock to deliver positive returns, even assuming that the investor reinvested any dividends distributed. Today, the stock is trading almost exactly at its 2000 peak.

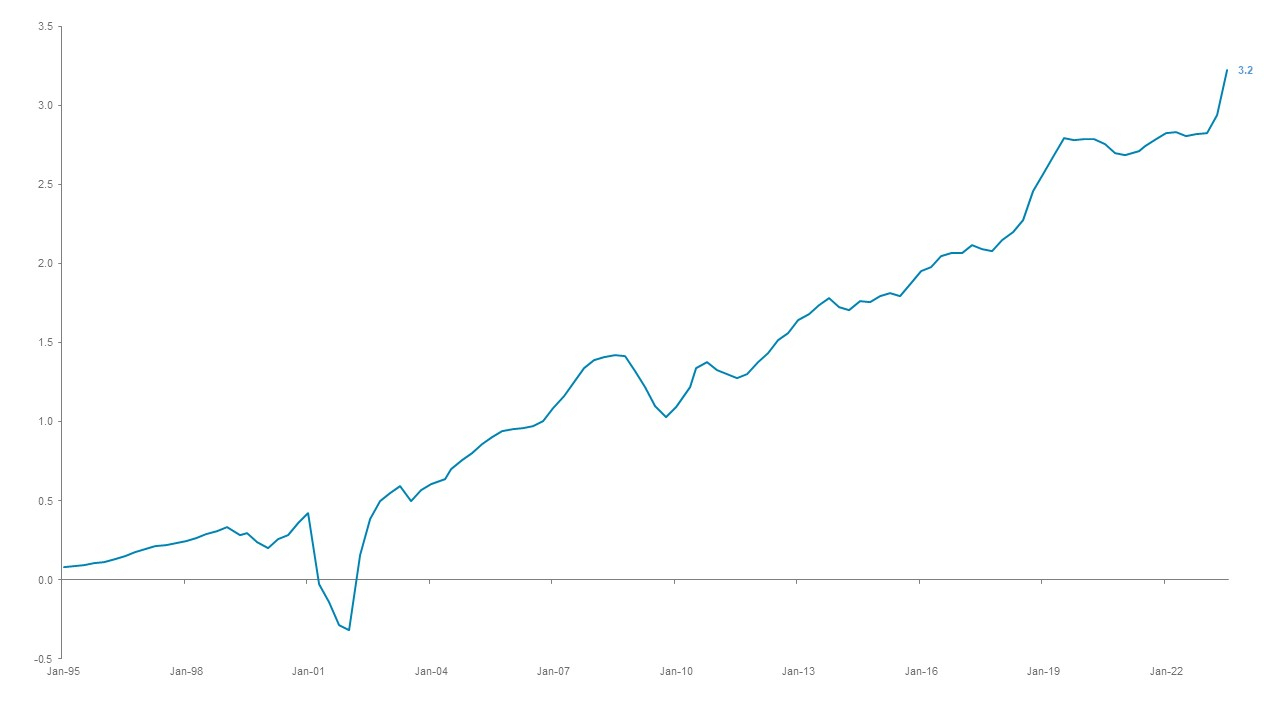

Was the stock’s performance a reflection of the company’s fortunes? To some degree yes. Earnings continued to grow into Q1 2001, but then fell into negative territory for the next year. However, by the end of 2002, trailing 12 months earnings hit a new record high and never really looked back. Since then, earnings have grown more than fivefold at a compound annual growth rate of 9-10 percent.

After a blip, Cisco’s earnings grew strongly over the next 2 decades

The challenge was not the company’s long-term outlook or doubts about the future of the internet, but the fervor with which investors extrapolated that outlook. In Q1 2000, the stock’s price-to-earnings ratio was over 250 times.

Fast forward to today and there is a risk we are about to see history repeat itself in another technology company. Before the latest earnings release, Nvidia’s price-to-earnings ratio, based on trailing earnings was over 220 times. This is not quite the nosebleed levels that we saw from Cisco, but it is not too far away. Of course, Nvidia earnings blasted above market expectations for the latest quarter and the consensus expects them to grow strongly into the future. Indeed, assuming forecasts for earnings to triple in 2024 prove correct, the price-earnings ratio would be a "mere" 45x.

Of course, what this does mean is a lot of the forecast growth is in the price already. It is, of course, possible the stock continues on a tear as the company outperforms market expectations. Valuations are rarely a useful predictive indicator for short term market performance. However, it does suggest that investors should be aware of the risks of a semi-permanent loss in value if they invest at current prices. If the company only doubles its earnings next year, let alone they decline, then the sell-off could be dramatic. Remember, Cisco as a company has performed very well over the past two decades, but 20 years is a long time for an investor to wait to get their money back.

So how should an investor operate in this environment? It is always critical to right-size any investment, but the narrower the investment, the more important this becomes.

We view investing through two lenses: foundation and opportunistic. I would place single stock holdings, especially stocks with the likelihood of significant volatility, in the opportunistic bucket. Investors should ask themselves, how they would feel if the stock went down, 20 percent, 50 percent or even 80 percent and then recovered only after decades. What would their brain tell them to do? If the answer is: "sell" (which is more likely), then a limited exposure to the stock would make sense. It should not be viewed as part of a foundational portfolio, but more as something on the opportunistic fringes, with the allocation accounting for a small fraction of the investor’s overall diversified portfolio.

Steve Brice is Standard Chartered Bank’s Chief Investment Officer. Views expressed in this article are his own. -- Ed.

-

Articles by Song Seung-hyun